How Affordable Are Homes These Days?

Rumor has it that first time buyers (thanks to the $8000 tax credit) and investors are making the bulk of home purchases these days. Like all savvy shoppers, I’m sure they want to make sure they are getting a good deal.

While, ultimately this is extremely personal calculation (because it depends on the buyer’s income, mortgage rates, how well the house will meet their needs, etc.) there is one generic indicator that we can use to get a sense of where the market is at overall: the Affordability Index.

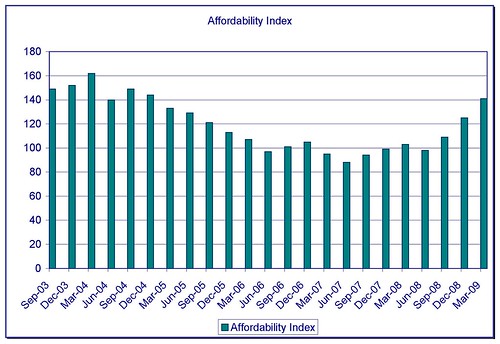

This graph shows the affordability index for the Portland Metro Area by quarter since Sept. 2003.

According to our calculations (which are based on a formula we got from the National Association of Realtors a while back) houses have been becoming increasingly more affordable since September 2008. But what does that mean?

Let’s look at the index rating for April, which was 1.41 (see graph above). In theory, someone making the median family income $70,000 according to HUD (surprisingly it’s up this year) would earn 41 percent more money than they would need to be able to afford the monthly payment on the median priced home in the Portland Market ($246, 400 according to the April 2009 Portland Market Action–of course).

That is IF they got a loan at the 4.81 percent average interest rate per Freddie Mac in April AND they had a 20 percent down payment (which we all know isn’t all that common for first time home buyers these days).

Question is: what will happen now that interest rates are starting to creep back up? We’ll let you know in the July issue of Market Action—that’s the next time we calculate and report affordability in the newsletter.